Global Omega-3 Supplements Markets: Channel shifts driving opportunity – and complexity

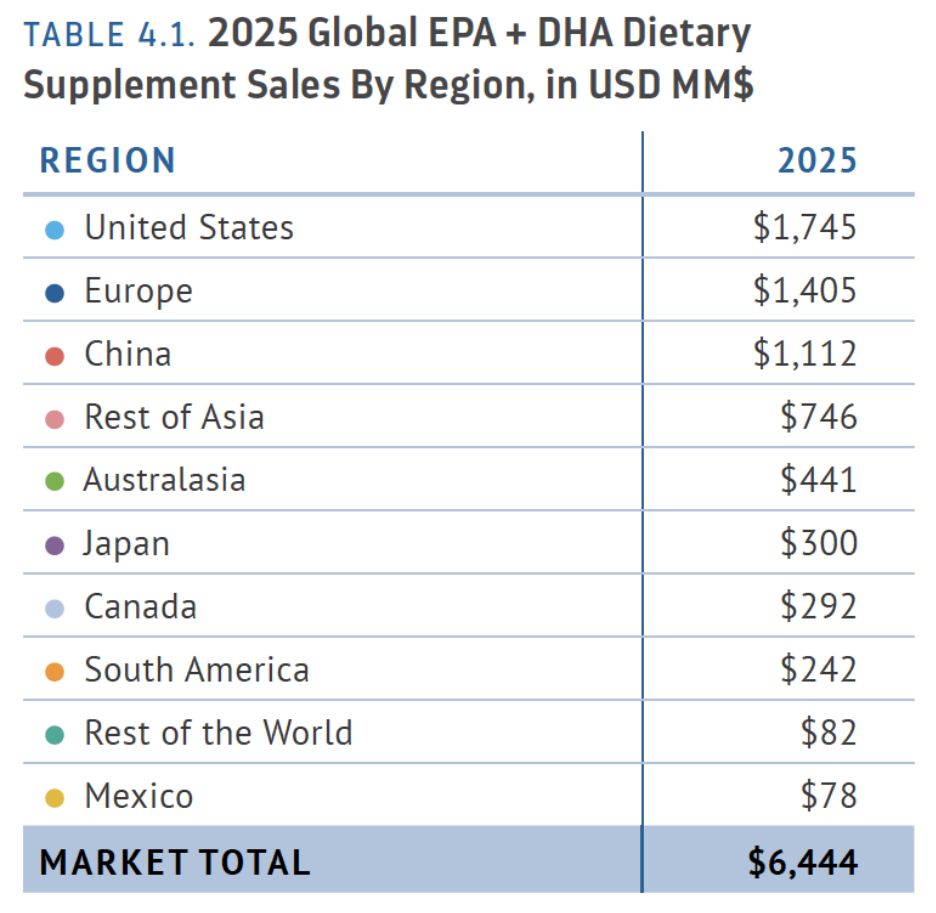

According to the newly published report ‘2026 Global EPA & DHA Finished Products Report’ by GOED, the global EPA/DHA supplement market reached approximately $6.4 billion in 2025, delivering 8.3% growth (following 7.0% in 2024). While supply constraints eased and supported recovery, the most important structural shift is happening in how products reach consumers, with channel evolution being a primary driver of both growth and competition.

E-commerce is the growth engine - but highly uneven

Online sales are expanding across all regions, but penetration varies sharply. In China and Japan, e-commerce accounts for up to 80% of sales, while South America and parts of Europe remain at 10–20%. North America sits between these extremes, but with strong momentum which is particularly driven by Amazon.

In the U.S. ($1.7B market, 27% of global share), growth of 8.3% in 2025 was closely tied to online expansion. Social commerce is also gaining traction, with approximately $1 billion in U.S. supplement sales now linked to social platforms.

Epax take on the data: Digital-first execution is no longer optional—but differentiation is critical as online channels accelerate price transparency.

China sets the benchmark for digital-led growth

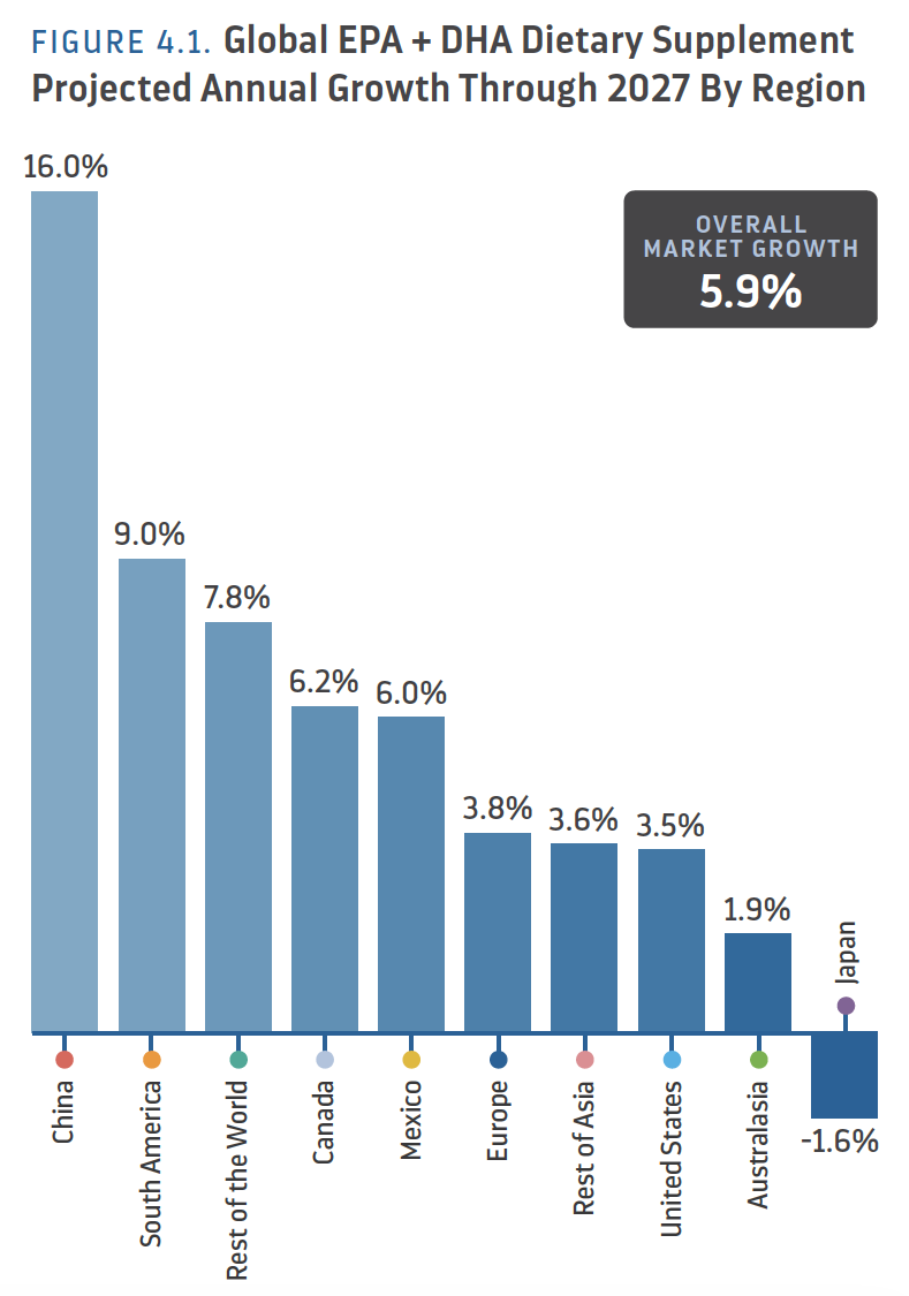

China ($1.1B, 17% of global share) grew 19.4% in 2025 and is forecast to reach $1.5B by 2027. The market is almost entirely platform-driven, with Tmall, JD.com, and Douyin dominating both discovery and conversion.

Consumer preferences are also highly specific: high-purity concentrates (>90%) and a 3:2 EPA:DHA ratio are considered standard.

Epax take on the data: There is a huge opportunity to scale rapidly through digital ecosystems and targeted formulations, but one must also consider the risk of intensifying competition and tightening regulatory scrutiny, particularly around claims and origin.

Europe and Australasia: slower channel shift, stronger retail legacy

Europe ($1.4B, 21% of global share) is growing more modestly at ~3.8%, with pharmacies still dominating distribution. E-commerce is expanding, but from a lower base, and fragmented regulations continue to slow cross-border scaling.

Australasia ($441M, 7% of global share) remains even more retail-driven, with <20% online penetration and strong reliance on chains like Chemist Warehouse. Growth of 6.5% in 2025 was largely price-driven, with a forecast slowdown to ~1.9%.

Epax take on the data: These are premium-driven markets where trust, quality, and retail presence still outweigh pure digital reach.

Asia (ex-China): mixed maturity, strong long-term upside

The rest of Asia ($746M, 12% of global share) is growing at ~3.6%, but masks major differences.

- South Korea: highly developed, with ~75% DTC penetration, but limited growth

- India & Southeast Asia: earlier-stage but expanding rapidly, driven by rising middle-class demand and interest in branded, high-quality products

Epax take on the data: There’s a solid opportunity for early positioning in high-growth markets now, but the risk is that fragmented regulatory environments and inconsistent channel infrastructure will complicate potential launches.

Japan and Canada: high structure, unique channel models

Japan ($300M, 5% of global share) is a mature, contracting market (-6.5% in 2024), where ~80% of sales are direct-to-consumer. Regulatory frameworks (FFC) favor high-dose, clinically substantiated products.

Canada ($292M, 4.5% of global share) is up +6.3%, and is notable for ~40% online penetration, driven largely by Amazon, and a higher share of liquid formats (10–15%) than most markets. However, strict regulatory approval processes slow innovation.

Epax take on the data: Both markets reward science-backed, differentiated products, but they require tailored channel strategies.

Latin America and Rest of World: high growth, high complexity

Latin America ($242M South America + $78M Mexico) is forecasted to continue its healthy growth, with pharmacies as the dominant channel and e-commerce (e.g., Mercado Libre) gaining share.

The “Rest of World” remains small ($82M, 1% of global share) but is expected to reach $95M by 2027, driven by expansion into emerging markets.

Epax take on the data: there is an opportunity for strong growth potential from low penetration, but with the risk being ability to scale due to fragmentation, regulatory diversity, and reliance on local partners.

Channel strategy is now core strategy

Across all regions, the direction is clear: growth is increasingly channel-led. E-commerce, social selling, and DTC models are expanding access, but also increasing competition, pricing pressure, and the need for clear positioning.

At the same time, fundamentals still matter. Fish oil accounts for >90% of products, softgels ~90% of volume, and while innovation (e.g., alternative formats representing 29% of new launches) is rising, success depends on combining quality, clarity, and accessibility.

Bottom line: The winners in omega-3 supplements will be those who align product, format, and messaging with the right channels, market by market, while maintaining trust in an increasingly transparent and competitive landscape.

Source: https://goedomega3.com/purchase-data-and-reports/fpr